The end of the year is a popular time for organizations to give their employees raises, with many of those raises taking effect in the new year. Increases in income are an ideal time to reassess, and if possible, increase your contribution to your retirement plan.

Increasing your contribution rate as your income grows is a key aspect to retirement planning. A key component of most people’s retirement plan is Social Security, however as your income grows, Social Security makes up less of your pre-retirement income, on a percentage basis. This difference will have to be made up through your private savings and/or pensions.

Increasing your contribution rate with pay raises can also help you catch up if you were unable to contribute as much as you would have liked to when you were younger. It can also help you get closer to reaching the maximum annual contribution.

Understandably, many are nervous about increasing their contribution rate throughout the year, because they do not want to decrease their take home pay. That is why timing an increase in contribution rate to coincide with an increase of income will often increase take home pay while also increasing retirement contribution, win-win!

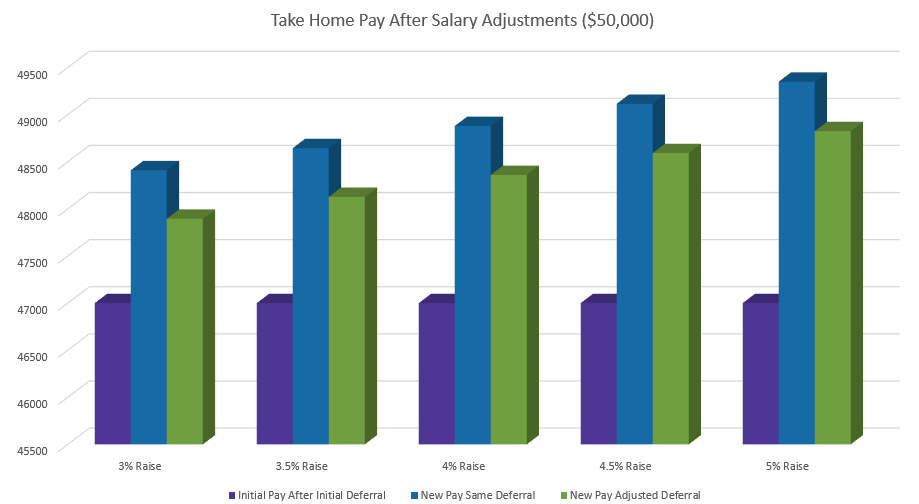

Consider someone initially earning an annual salary of $50,000 and contributing 6% of their salary to their retirement plan. Below is a graph describing ten scenarios, in which they receive a raise between 3% and 5%, and for each raise they either keep their current contribution rate at 6% or increase it to 7%.

*This graph does not consider inflation, taxes, or other benefits, and is meant to be illustrative.*

In each scenario, the net pay after increasing the worker’s salary and deferral rate is considerably more than their previous net pay, and fairly close to the net pay of someone who kept their deferral rate the same.

A larger salary increase coupled with a 1% increase retirement plan deferral can increase both net take home pay and the total amount that you are contributing for your retirement. With some forward planning, you can even set your increase to take effect on the same pay period that your salary increase takes effect. That way, you can maximize the amount that you contribute while also not getting used to the new pay with the old deferral rate.