In August, the yield curve on US Treasuries inverted. Often, this is viewed by investors as a recessionary signal.

Although an inverted yield curve is not always a reliable predictor of recession, the thought of recession brings up fear for many people. For people in the workforce prior to 2008-09, this brings back many fears, and for people who entered the workforce in the last 10 years, it can be equally unnerving. In terms of saving for retirement, the question on a lot of people’s minds is “how should I prepare my retirement portfolio for a potential recession?”

First, keep contributing to your retirement accounts. Some investors think they should slow or cease contributions while the market is going down. The dollars that you put in at the bottom of the market are the dollars that are going to grow the most during recovery. Also, if your employer matches contributions, ceasing your contribution will cause you to leave free money on the table. If your other needs are being met, there is no reason to stop contributing or waiting for a “better” time to contribute.

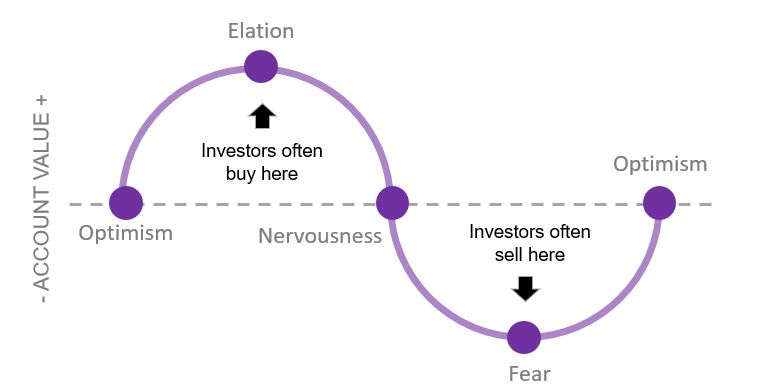

When predictions of recession arise, many people think about temporarily moving their retirement portfolio to a more conservative allocation. While a more conservative portfolio might do better in a recession, in changing your asset allocation temporarily you run the risk of mistiming the market. That is, you may end up buying back into the market at a price that is higher than what you sold at. The chart below shows some of the emotions that come with market fluctuations, and how short-term decisions can lead to mistiming the market.

Instead of trying to time the market based on fears of recession, the fear of recession should be built into your asset allocation—just as periods of growth should be. It can be very difficult to stick with your investment strategy, especially during market downturns. Emotion can drive short-term investment decisions, and it is important to remember that your retirement savings are for the long term.