Given the significant current level of inflation and recent declines in stocks and bonds, how should an investor position their portfolio?

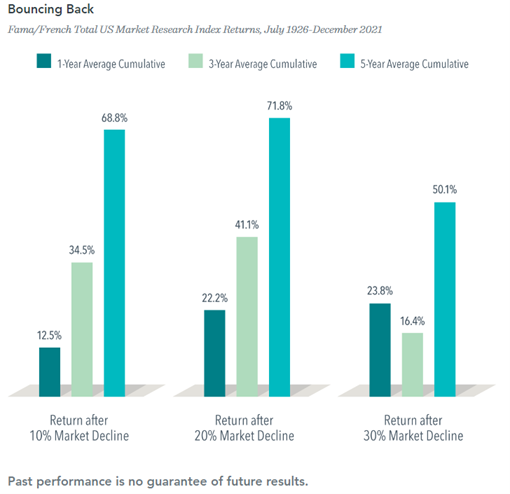

First and foremost, we think an investor is best served by remaining disciplined to their investment strategy. Fleeing the stock market and moving to cash “until there is less uncertainty” is unlikely to work out for an investor. Only by remaining invested can you benefit from the expected long term returns from stocks. Recoveries can also happen quickly. As can be seen in the below chart, the broad US stock market has on average offered positive returns in the one-year, three-year and five-year time periods after steep declines.

Also on the stock side of the portfolio, if an investor does not have other preferences that take precedence, we recommend maintaining an emphasis to value stocks. Value stocks are those that have a relatively lower price for a given level of earnings. Value stocks have performed very well historically rising 12.8% since 1926 through April 2022 as measured by the Fama/French US Value index, compared to the S&P 500 which has gained 10.3% over the same time. In addition, value stocks, often perform well in inflationary environments because their revenue is typically more near term compared to growth stocks whose revenue is more frequently further out in the future. As a result, inflation does not erode value stocks’ earnings and therefore those companies’ valuations as much.

This has been the case since inflation started to significantly climb in April of 2021. Another point of comparison is the 1970’s and early 80’s when the Consumer Price Index averaged 7.3% from 1970 through 1983. As can be seen below, value stocks have significantly outpaced growth stocks over both time periods as measured by the Fama/French US Value and Growth indices.

Value vs Growth Annualized Performance |

| January 1970 through December 1983 | April 2021 through April 2022 | |

| Fama/French US Value | 16.23% | 12.83% |

| Fama/French US Growth | 6.99% | 0.80% |

On the bond side of the portfolio, we recommend keeping the portfolio shorter term than the broad bond market. Shorter term bonds mature sooner and can be reinvested in current, higher yielding bonds faster. The newly issued bonds are factoring in current inflation expectations, so if inflation expectations rise, yields would likely rise as well.

In addition, for both stocks and bonds, it is important to diversify the portfolio internationally. Different regions of the world are experiencing different stages of the business cycle and different inflation conditions and thus different stock and bond market environments. We have seen many large economics, notably China, Japan, France, Canada, and Germany, post lower inflation rates this year than that in the US. By investing abroad, you do not limit your portfolio to how the US is performing. While the US has performed well in recent years, international stocks, as defined by the FTSE All World Ex US Index, have outpaced US stocks, as defined as the Russell 3000 Index, by 5.25% for the year to date through 6/13.

No one knows what the future holds for the markets. The Fed is aggressively trying to bring down inflation, but how quickly they can make an impact is an open question. Markets are likely to remain highly volatile driven by inflation until there is clear evidence of it moderating. In this environment we believe that investors are best served by remaining disciplined to their portfolio’s target allocation strategy, emphasizing value stocks when possible, emphasizing a shorter term bond allocation then the broad bond market and diversifying the stock and bond side of the portfolio internationally. We believe taking these steps will help cushion the blow from the current bout of high inflation and set up investors for long term investment success.