Key Takeaways:

- An Outsourced Chief Investment Officer (OCIO) is typically a discretionary investment management arrangement in which an external adviser may be authorized to implement investment decisions within guidelines set by the board.

- In a non-discretionary model, the adviser recommends and the board approves each decision. In a discretionary model, the board sets policy and the adviser executes.

- Discretionary structures are often selected by nonprofits because they may support more consistent implementation, timelier decision‑making, and clearer role definition, depending on the organization’s governance and oversight practices.

- The right structure depends on your organization’s governance capacity, the experience of your decision-makers, and the complexity of your investment program.

What is an OCIO?

An Outsourced Chief Investment Officer (OCIO) is typically a discretionary investment management arrangement in which an external adviser may be authorized to implement investment decisions within guidelines set by the board. The term has become a popular way to describe this approach, but at its core, it is simply a framework for how responsibilities are divided between the board and the adviser.

For many nonprofit organizations, selecting an investment advisor raises an important but often underexplored question: Who is actually making the investment decisions?

This question sits at the center of the distinction between discretionary and non-discretionary investment management, and it is also where the concept of an Outsourced Chief Investment Officer (OCIO) comes into play.

Understanding how these structures differ can help organizations make more informed decisions about how their investment program should function in practice.

Discretionary vs. Non-Discretionary Investment Management: What Is the Difference?

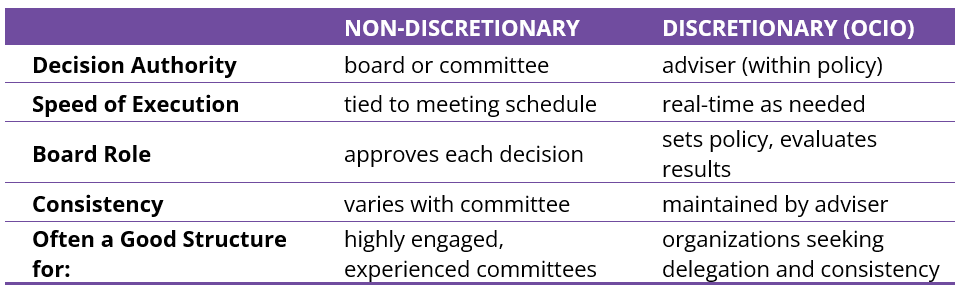

The distinction between discretionary and non-discretionary investment management comes down to who has authority to act.

In a non-discretionary structure, the advisor provides recommendations, but the board or investment committee retains responsibility for approving each decision before it is implemented.

In a discretionary structure, the advisor is authorized to implement decisions within the parameters defined by the organization’s investment policy. The board maintains oversight, but day-to-day decisions are delegated.

Both approaches can be appropriate in different circumstances. The key is understanding how each structure affects decision-making over time.

How Investment Decisions Get Made in Each Model

Non-Discretionary Investment Management

In a non-discretionary model, every investment decision requires board or committee approval before it can be implemented. The process typically looks like this:

- The advisor makes a recommendation

- The board or committee reviews it

- A decision is made at a meeting (or between meetings)

- The advisor implements the approved action

This structure provides direct involvement, but it can also introduce delays and make it more difficult to act consistently, particularly when markets are moving quickly or when decisions require timely execution. This can be particularly challenging for organizations whose committees have limited bandwidth that restricts them from making timely decisions.

Discretionary Investment Management

In a discretionary model, the adviser is able to make decisions and update the portfolio quickly, as long as the decisions are in line with the defined investment policy. The process typically looks like this:

- The board defines the investment policy and overall strategy

- The advisor implements decisions within those guidelines

- The board evaluates results over time

This creates a clearer separation between policy and oversight on one hand, and implementation on the other.

What Does an OCIO Actually Do?

When evaluating if hiring an OCIO would be beneficial to your organization, it is helpful to understand what an OCIO is and how they would support your nonprofits investment management program. The discretionary investment management model is often referred to as an Outsourced Chief Investment Officer (OCIO) approach. Through this structure, the advisor effectively supports and executes the organization’s investment function, subject to board oversight, handling responsibilities that include:

- Portfolio implementation

- Rebalancing and adjustments

- Manager selection (if applicable)

- Ongoing monitoring and execution

At the same time, the board and committee retain responsibility for:

- Setting investment policy

- Defining objectives and constraints

- Evaluating results

- Maintaining oversight

In other words, the OCIO model is less about a specific product or strategy, and more about how responsibilities are divided. It gives nonprofit organizations access to professional investment management while keeping governance where it belongs: with the board.

Why Many Nonprofits and Associations Choose a Discretionary (OCIO) Structure

In practice, many nonprofits and associations choose a discretionary or OCIO model for a few practical reasons.

Consistency Over Time

Volunteer boards and committees naturally change over time. A discretionary structure may help support more consistent implementation of the investment strategy, regardless of who is serving in a governance role at any given moment.

Timely Decision-Making

Markets do not move on a meeting schedule. Delegating policy implementation to an experienced investment adviser allows decisions to be made when needed, rather than waiting for the next committee meeting. This can be particularly challenging for organizations whose committees meet infrequently, are slow to reach consensus, or have members with limited availability between meetings. Under a discretionary model, the adviser can respond to changing market conditions without waiting for committee approval.

Clearer Roles

One of the most important benefits is clarity.

- The board focuses on policy and oversight

- The advisor focuses on execution and implementation

For nonprofit and association boards where committee members are volunteers and may not have investment backgrounds, this clarity is particularly valuable. It allows board members to focus on the questions they are best positioned to answer, such as risk tolerance and organizational priorities, rather than individual security or manager selection decisions.

A More Durable Process

A well-defined structure helps support a more disciplined approach over time, which is often more important than any individual decision.

The Role of Reporting and Oversight

Regardless of which model an organization chooses, regular and detailed reporting is what allows the board to fulfill its oversight responsibilities. In a non-discretionary model, reporting helps the committee evaluate recommendations and make informed decisions. In a discretionary model, reporting becomes even more important because it is the primary way the board monitors whether the adviser is managing the portfolio in line with the guidelines set out in the Investment Policy Statement.

Strong reporting should clearly show what changes have been made to the portfolio, why those changes were made, and how the portfolio is performing relative to the benchmarks defined in the IPS. This level of transparency is what allows a board to delegate with confidence and maintain informed oversight. It is also one of the reasons the Investment Policy Statement itself is so important. The IPS defines the framework the adviser is operating within. Without a clear, well-constructed IPS, there is no standard against which to measure whether the adviser is doing what the organization agreed to.

When evaluating advisory firms, it is worth asking how they approach reporting, how frequently reports are delivered, what level of detail they include, and how clearly changes are tied back to the investment policy. The quality of reporting is one of the most practical indicators of how well the advisory relationship will work over time.

OCIO and Fiduciary Responsibility: What Nonprofit Boards Should Know

It is natural to ask how these structures relate to fiduciary responsibility. In general, frameworks for fiduciary best practices emphasize:

- Engaging qualified advisors through a thoughtful process

- Clearly defining roles and responsibilities

- Delegating authority appropriately

- Maintaining ongoing oversight

When these elements are in place, organizations are better positioned to demonstrate a prudent and well-governed investment process.

It is important to note that fiduciary responsibility is not eliminated under any structure. The board retains ultimate responsibility for oversight and for verifying that the investment program remains aligned with the organization’s objectives.

There is also a practical difference in how fiduciary risk is distributed under each model. In a non-discretionary structure, the board or investment committee is more directly involved in each decision, which means it carries a greater share of the responsibility for those decisions. In a discretionary structure, the adviser assumes greater responsibility for implementation, while the board retains ultimate fiduciary oversight. This is one reason some advisory firms charge more for discretionary engagements. When evaluating advisers, it is worth understanding how each firm structures its fees relative to the level of responsibility it is taking on.

Is a Discretionary (OCIO) Structure Right for Your Organization?

It depends. Some organizations prefer to retain direct control over all investment decisions, particularly if they have:

- A highly engaged and experienced investment committee

- The ability to meet frequently

- A preference for hands-on involvement

In these cases, a non-discretionary structure can work well. The key is alignment and the structure should reflect:

- The organization’s governance capacity

- The experience and availability of decision-makers

- The complexity of the investment program

You may want to consider a discretionary or OCIO structure if your board or investment committee has limited time or bandwidth for investment decisions, if committee membership changes frequently, if your investment program has grown in complexity, or if you want decisions and portfolio updates to be made in a timely manner, even between meetings.

How to Choose the Right Investment Management Structure

The decision between discretionary and non-discretionary investment management is not just a technical detail. It is a foundational choice that shapes how an investment program operates day to day.

The OCIO investment consulting model is one way of structuring that relationship, but at its core, the question is simpler: How should investment decisions be made, and by whom?

Organizations that answer and define this question clearly are better positioned to maintain discipline, support effective oversight, and work toward an investment strategy that continues to serve their long-term objectives.

Working with an adviser who understands how nonprofit and association boards operate can help bring clarity to that conversation. Raffa Investment Advisers works with nonprofits in both discretionary (Outsourced Chief Investment Officer) and non-discretionary investment management arrangements. Our objective is to help organizations develop comprehensive investment programs that are aligned with their long-term objectives.

Frequently Asked Questions: Nonprofit & Association Investment Management

What is an OCIO?

An Outsourced Chief Investment Officer (OCIO) typically represents an external investment adviser working within a discretionary investment management arrangement. Within this arrangement, the adviser is typically authorized to implement investment decisions within guidelines set by the nonprofit or association’s investment policy statement (IPS). The board retains investment oversight and is responsible for defining the investment policy. The adviser handles day-to-day execution.

What is the difference between discretionary and non-discretionary investment management?

In a non-discretionary model, the adviser typically recommends and the board approves each decision before it is implemented. In a discretionary model, the board sets the investment policy and the adviser typically implements decisions within those guidelines. The discretionary model is often referred to as an OCIO approach.

Is an OCIO a fiduciary?

Fiduciary responsibility depends on the specific advisory relationship, not the structure or arrangement itself. In an OCIO model, the board retains ultimate fiduciary responsibility for oversight. The adviser operates within the authority granted by the investment policy. When roles are clearly defined and oversight is maintained, both the board and the adviser are positioned to fulfill their respective fiduciary obligations.

When should a nonprofit or association consider an OCIO?

Organizations often consider an OCIO, or a discretionary investment management structure, when their investment committee has limited bandwidth, when committee turnover is frequent, when their investment program has grown in complexity, or when they wish to delegate decision-making (in line with the investment policy). An OCIO structure or discretionary structure can help support consistency, timely decision-making, and a clearer separation between governance and implementation. There are benefits to both discretionary and non-discretionary investment advisory arrangements that should be carefully considered before selecting an approach for your organization.

What does Raffa Investment Advisers do for nonprofits and associations?

Raffa is an investment advisory firm purpose-built to serve nonprofit organizations and associations. We work directly with finance committees and executive leadership on investment policy development, reserve strategy, investment management, board education, and more. We currently serve more than 174 nonprofit and association clients nationwide. Additionally, our firm supports clients through both discretionary (OCIO) and non-discretionary investment management structures.

Schedule a meeting with Raffa Investment Advisers to learn more.

Is an OCIO right for mid-sized nonprofits and associations?

Yes. The OCIO model is not limited to large institutions with billion-dollar endowments. Many mid-sized nonprofits and associations find that a discretionary structure is a natural fit, particularly when their investment committee has limited bandwidth, when committee members rotate frequently, or when the organization simply wants a more consistent and professionally managed investment process. In fact, mid-sized organizations often benefit the most from this model because they are large enough to have meaningful reserves that need active management, but not large enough to justify a full-time internal investment team. The key is finding an adviser who understands the specific needs of organizations your size and is structured to serve them well, rather than treating you as a smaller version of a much larger client.

Does an OCIO replace the Finance Committee or Investment Committee?

No. An OCIO does not replace a finance committee or an investment committee. It changes what the committee spends its time on. Instead of reviewing and approving individual investment decisions, the committee focuses on setting the investment policy, defining the organization’s objectives and risk tolerance, evaluating performance, and maintaining oversight of the overall program. For many committees, this shift actually makes their time more productive and their role more meaningful. They spend less time on implementation details and more time on the strategic and governance questions they are best positioned to address. The committee remains essential. The OCIO model simply gives it a clearer, more focused mandate.

Can a Nonprofit or Association switch between non-discretionary and discretionary (OCIO) investment management?

Yes. Nonprofits and associations can move between non-discretionary and discretionary investment management arrangements, and some organizations do so as their needs evolve. The process in either direction typically starts with the board or investment committee evaluating whether the current structure still reflects how the organization wants investment decisions to be made. Moving to a discretionary model generally involves establishing or updating the Investment Policy Statement to define the guidelines the adviser will operate within, then formally authorizing the adviser to implement decisions within those parameters. Moving to a non-discretionary model involves pulling that authority back to the board or committee, so that the adviser returns to a recommendation-and-approval process. In either case, a well-constructed IPS remains the foundation, because it defines the objectives, risk parameters, and benchmarks that guide the program regardless of which model is in place.

Dennis Gogarty, CFP®, AIF®

President & Co-Founder

Dennis Gogarty, CFP®, AIF® is President and Co-Founder of Raffa Investment Advisers, a firm he purpose-built to serve nonprofit organizations and membership associations. For more than 20 years, he has advised nonprofits and associations on fiduciary-focused reserve strategy, investment policy development, asset allocation, and governance best practices. Raffa currently serves more than 174 nonprofit clients nationwide (as of December 31, 2025). Dennis is a frequent speaker for nonprofit and association audiences and has presented for numerous organizations including the Council on Foundations, AICPA, BoardSource, and the American Society of Association Executives (ASAE).

Disclosures:

Raffa Investment Advisers (Raffa) is a registered investment adviser. Registration with the U.S. Securities and Exchange Commission does not imply a certain level of skill or training. This material is provided for informational and educational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security.

The information contained herein is general in nature and does not take into account the specific objectives, financial situation, or needs of any particular organization. Advisory services are provided only pursuant to a written advisory agreement. Investment strategies and governance structures discussed may not be suitable for all organizations, and no investment decision should be made based solely on this material.

References to discretionary investment management or Outsourced Chief Investment Officer (OCIO) services are intended to describe general industry practices. The specific scope of an adviser’s authority, responsibilities, and fiduciary obligations is defined by the applicable advisory agreement and investment policy statement. Regardless of the investment management structure selected, an organization’s board or governing body retains ultimate fiduciary responsibility for oversight of the investment program.

Any discussion of potential benefits associated with discretionary or non discretionary investment management structures is illustrative and not a guarantee of outcomes. Organizational governance effectiveness, decision making efficiency, and investment results depend on many factors and cannot be assured.

All investments involve risk, including the potential loss of principal. Past performance is not indicative of future results.

Raffa actively leverages Artificial Intelligence (“AI”) and Large Language Models (“LLMs”) within our operations. The use of such technologies, focusing on the safeguard of non-public personal information (“NPPI”), protecting of trade secrets, verification of information accuracy, and other pertinent compliance considerations, is outlined in Raffa’s Compliance Manual and acknowledged by Raffa staff. All viewpoints and final content created was reviewed and approved by the Raffa team to verify accuracy, perspective, and compliance with our marketing guidelines.